What to look for in a portfolio tracker

Short answer: A good portfolio tracker should consolidate every account in one view, separate contributions from gains, surface your real fees and asset allocation, handle Canadian account types (TFSA, RRSP, FHSA), and track adjusted cost base. Balance aggregation alone isn’t enough.

I’ve tried a lot of portfolio trackers. Spreadsheets, apps, brokerage dashboards, even a notes app at one point (don’t judge). Most of them did the same thing: they showed me a number. My balance today. Maybe a chart going up or down. That was it.

But knowing your balance isn’t the same as knowing how your portfolio is doing. A balance tells you what you have. A real portfolio tracker tells you what’s working, what it’s costing you, and whether you’re actually on track. If you’re shopping for a tracker or wondering whether your current one is doing enough, here’s what I’d look for.

Knowing your balance isn’t the same as knowing how your portfolio is doing.

Multi-account consolidation

If you’re like most Canadian investors, your money isn’t in one place. You’ve got a TFSA here, an RRSP there, maybe a non-registered account at a different brokerage, and your spouse has their own set of accounts on top of that. Checking each one individually and trying to piece together the full picture in your head doesn’t work. You end up with a rough idea at best.

A good tracker should let you see everything in one view. All your accounts, all your brokerages, all in one place. Without this, you’re always working with incomplete information. You might think you’re well diversified, but if you can’t see your full portfolio at once, you’re guessing. This is the multi-account problem, and it’s one of the first things that separates a real tracker from a balance checker.

Canadian tax awareness

This one matters more than most people realize. If you’re using a tool built for American investors, it has no concept of a TFSA. It doesn’t understand that gains in your RRSP are taxed differently from gains in a non-registered account. It probably doesn’t track your adjusted cost base (ACB) the way the CRA expects.

ACB tracking is especially important if you hold investments outside of a registered account. Every time you buy, sell, reinvest a distribution, or receive a return of capital, your ACB changes. Getting it wrong means reporting the wrong capital gain or loss on your taxes. Most brokerages don’t track this perfectly for you, and a U.S. tool certainly won’t.

If you invest in Canada, your tracker needs to understand Canadian tax rules. That means registered vs. non-registered distinctions, proper ACB calculations, and awareness of how things like return of capital affect your cost base. There’s a full breakdown of how ACB works if you want to dig deeper.

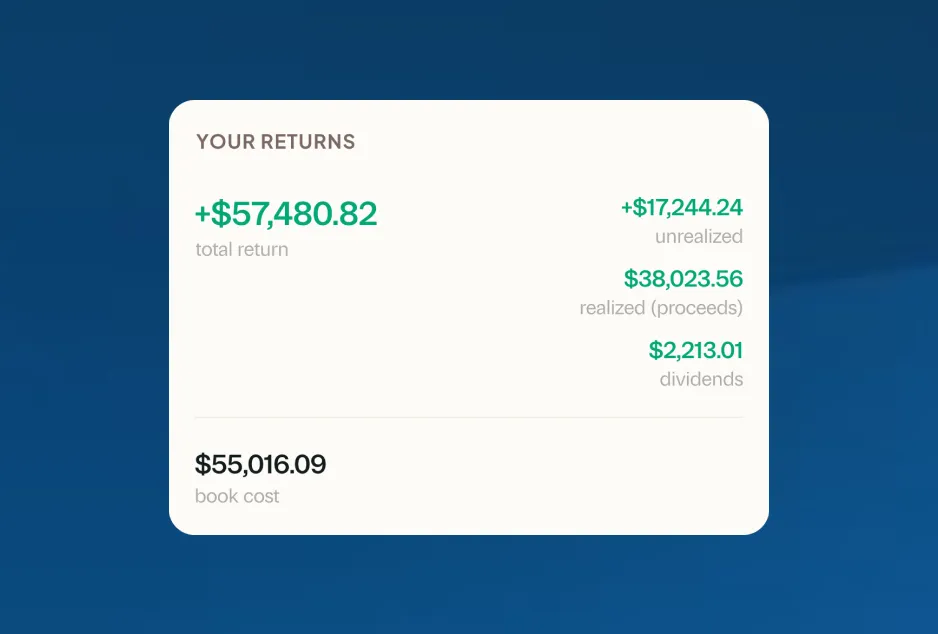

Return calculations that mean something

Your brokerage might tell you you’re “up 12%.” But up 12% how? Is that since you opened the account? This year? And does it account for the money you added along the way, or is it just comparing two balances?

There are two main ways to calculate returns: time-weighted and money-weighted. Time-weighted returns show how your investments performed regardless of when you added or withdrew money. Money-weighted returns reflect the impact of your actual cash flow decisions. Both are useful. Neither is the one your brokerage usually shows you, which is often just a simple gain/loss number that mixes contributions with actual returns.

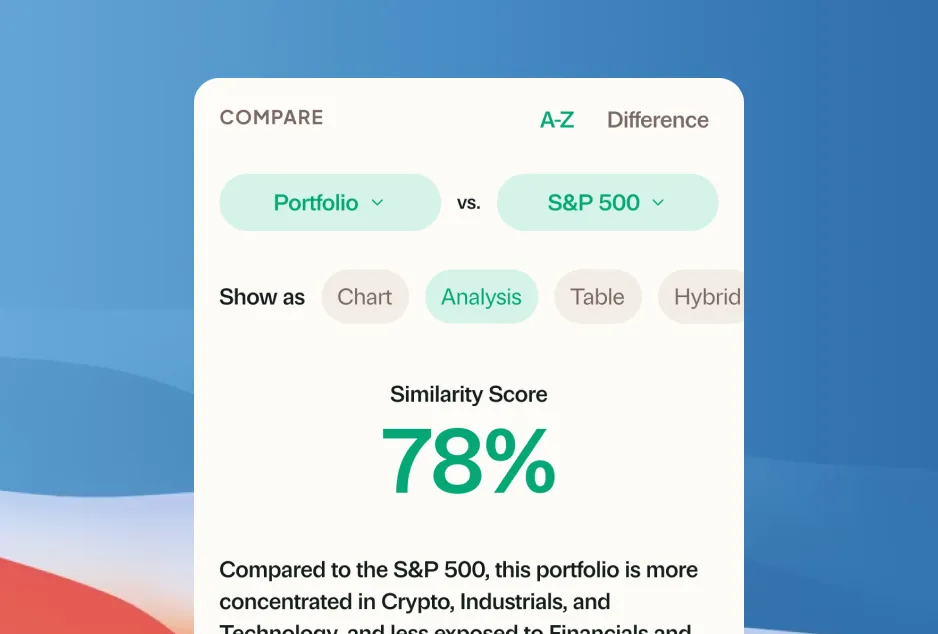

A proper tracker should separate your contributions from your investment returns. It should let you see both time-weighted and money-weighted performance, and ideally let you compare against a benchmark so you know whether your picks are actually doing better than a simple index fund. If you’re curious about why this gets confusing, I wrote about why investment returns are so hard to understand.

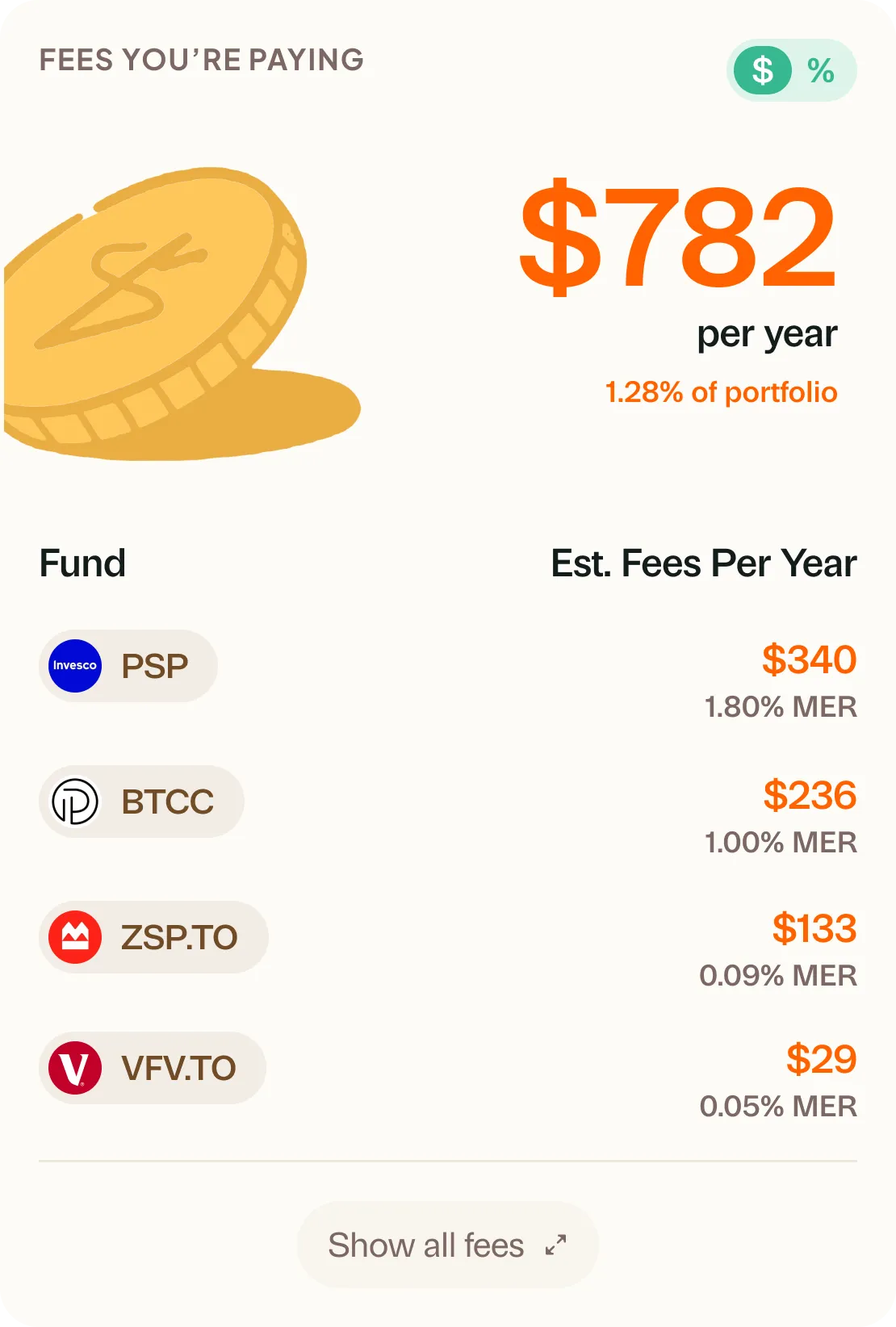

Fee visibility

Fees are the one thing in investing you can actually control. You can’t control the market, you can’t predict which stock will go up, but you can choose funds with lower fees. The problem is, most tools don’t make fees visible at all.

A good tracker should show you the MER on every fund you hold and calculate the total dollar amount you’re paying in fees across your entire portfolio. Not just the percentage, the actual dollar figure. When you see that you’re paying $1,800 a year in fees on a $100,000 portfolio, it hits differently than seeing “1.8%.” If fees aren’t something you’ve looked into before, here’s where your money might be going.

How it handles your data

This is a question more people should ask. Does the tracker require your bank login to pull data? If so, where are those credentials stored? Who has access?

Some trackers use screen scraping or credential sharing to connect to your brokerage. Others let you enter your data manually or import from files. There are real tradeoffs here, and it’s worth understanding what you’re giving up for the sake of convenience. I wrote a whole piece on why portfolio trackers want your bank login and what to consider before handing over access.

Currency handling

A lot of Canadian investors hold U.S. stocks or U.S.-listed ETFs. If your tracker doesn’t handle currency properly, your portfolio value will be wrong. Sometimes very wrong.

Good currency handling means converting USD holdings to CAD at the correct exchange rate, updating that rate regularly, and ideally showing you both the CAD and USD values side by side. It also means your return calculations should account for currency fluctuations. If the S&P 500 was flat but the Canadian dollar weakened, your USD holdings actually went up in CAD terms. A tracker that ignores currency is giving you the wrong picture.

Account type awareness

TFSA, RRSP, RESP, LIRA, FHSA, non-registered. These aren’t just labels you slap on an account. Each one has different contribution rules, withdrawal rules, and tax treatment. The gains in your TFSA are completely tax-free. The gains in your non-registered account are taxable. Your RRSP withdrawals get added to your income.

A Canadian portfolio tracker should understand these differences. It should know that selling something in your TFSA has different tax implications than selling the exact same thing in your non-registered account. If the tracker treats all your accounts the same way, it’s missing something important. These distinctions affect everything from your return calculations to your contribution room to your tax planning.

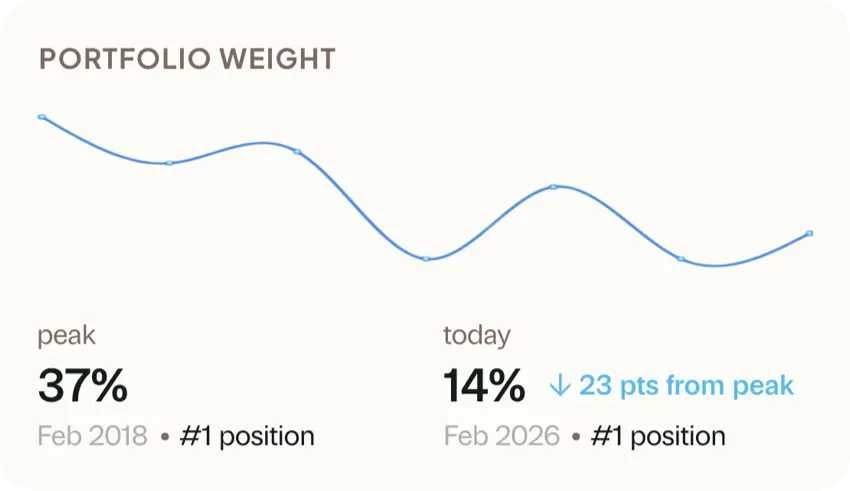

Portfolio weight and allocation

Owning a dozen ETFs across five accounts doesn’t tell you much on its own. What matters is how those holdings add up. What percentage of your total portfolio is in Canadian equities? How much is in bonds? Are you overweight in one sector without realizing it?

A good tracker should show you your actual allocation across everything. Not just within one account, but across all of them combined. Sector breakdown, geographic exposure, asset class split. This is how you spot imbalances and make informed decisions about what to buy next. Without this view, you might be doubling up on the same exposure across multiple accounts without knowing it.

Does a free portfolio tracker work as well as a paid one?

It depends on what you need. Free tools typically cover the basics: listing your holdings, showing your balance, maybe a simple chart. If that’s all you want, free works fine.

Where paid trackers tend to pull ahead is in the details. Proper ACB tracking, fee analysis, multi-account consolidation, Canadian tax awareness, benchmark comparisons. These features take real work to build and maintain, especially for the Canadian market. If you’re serious about understanding your investments and not just checking a number, it’s worth looking at what you get for the price.

What’s the most important feature in a portfolio tracker?

Consolidation. If you can’t see everything in one place, every other feature is working with incomplete data. Your allocation numbers are wrong because they only reflect one account. Your return calculations are off because they don’t include that RRSP at another brokerage. Your fee analysis misses half your holdings.

Getting everything into a single view is the foundation. Once you have that, features like tax awareness, return calculations, and fee analysis become genuinely useful. Without it, you’re making decisions based on partial information, and that’s no better than guessing.

If you want that single consolidated view without handing over your bank login, that’s the problem we built Greenline to solve.

More in The Long Game

Best way to track your portfolio in Canada

Why most portfolio trackers want your bank login

What you're actually paying in investment fees

Best way to track your portfolio in Canada

We built a portfolio tracker, so we're biased. But here's an honest look at every approach: spreadsheets, brokerage tools, bank-linked apps, and more.

Why most portfolio trackers want your bank login

What you're actually paying in investment fees

See what a real portfolio tracker looks like

See your full portfolioFree during Beta. Early Members will be offered better rates than new users when we launch paid plans.