Do you even need a portfolio tracker?

Short answer: Probably not, if you have one account holding one all-in-one ETF. A tracker starts to matter once you have multiple accounts, multiple brokerages, individual stocks, or non-registered holdings where adjusted cost base, fees, and tax start to add up.

I built a portfolio tracker, so you’d expect me to say yes. But the honest answer is: it depends. Some people genuinely don’t need one. If that’s you, I’d rather you know now than sign up for something that doesn’t help.

That might sound strange coming from someone who spent years building one. But the reason I built Greenline wasn’t because every investor needs a separate tool. It was because I hit a point where my brokerage apps couldn’t answer basic questions about my own money. Not everyone reaches that point. And if you haven’t, there’s nothing wrong with keeping things simple.

When your brokerage app is enough

If you have one account at one brokerage and you hold a single all-in-one ETF like XEQT or VGRO, your brokerage app is probably doing everything you need. You check it once a quarter, you see a balance, and you move on. That’s good investing. Most of it is just not touching things.

Seriously. If your entire investing strategy is “contribute regularly to a TFSA, buy one ETF, don’t look at it too often,” you’re ahead of most people. A portfolio tracker would just be another app on your phone showing you roughly the same number your brokerage already shows you.

There’s no prize for complexity. If your situation is simple and you’re comfortable with what your brokerage provides, stay there. The goal is to make good decisions, not to use more tools.

There’s no prize for complexity in investing. If your setup works, don’t add more tools just because they exist.

When it starts to break down

The cracks usually start showing when a second account enters the picture.

Maybe you opened a TFSA at one brokerage because a friend recommended it, and then your employer set up a group RRSP at a different institution. Now you have two accounts at two different places, each with its own login and its own dashboard. Neither one knows the other exists.

Then your spouse has their own accounts. Maybe a taxable account shows up because you’ve maxed your registered room. Suddenly, your “simple” investing life involves four or five accounts across three platforms, and no single screen shows you what you actually own across all of them.

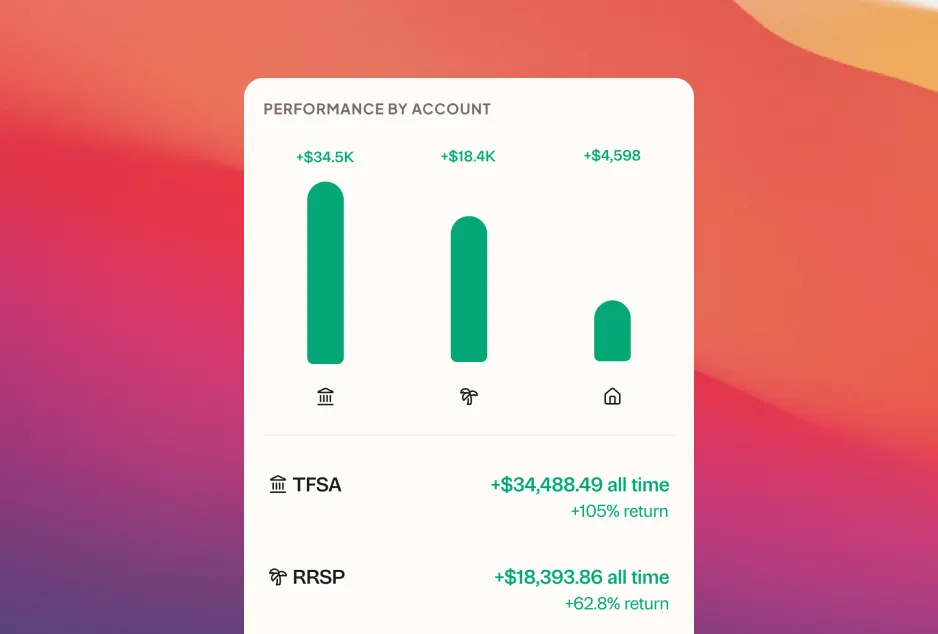

This is the multi-account problem. Each account looks fine on its own. But you can’t see your real allocation, you can’t spot overlap, and you can’t answer basic questions like “how much of my total portfolio is in Canadian equities?” without opening every app and doing math on paper. That’s where a tracker stops being a nice-to-have and starts being genuinely useful.

The “how am I actually doing” moment

For a lot of people, the real trigger isn’t complexity. It’s a question.

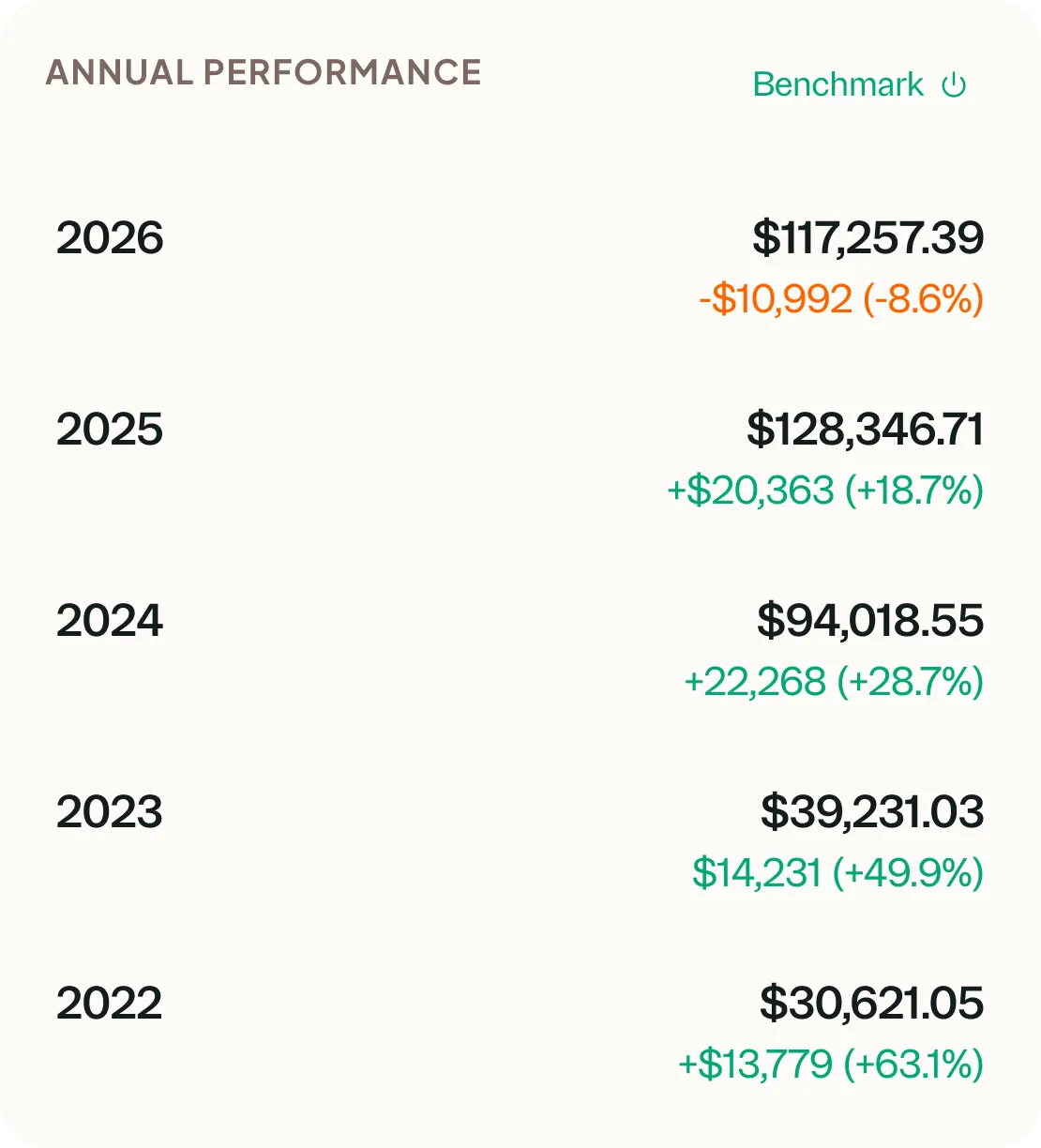

You’re a few years into investing. Someone asks how your portfolio did last year. You open your brokerage app, see a number, and realize you don’t actually know if it’s good or bad. The app shows your balance went up, but you also deposited money throughout the year. How much of that increase was growth? How much was just your own contributions landing in the account? You genuinely can’t tell.

That’s the moment. You want to know your real return, separated from the cash you added. You want to compare your performance against a benchmark. You want to see if your decisions over the past three years actually made a difference, or if you would have been better off in a single index fund. Your brokerage doesn’t show you any of this. It just shows you a balance and maybe a percentage that you’re not sure how to interpret.

This is what I wrote about in do you know how your portfolio is actually doing. It’s the gap between feeling like things are going well and actually knowing. A tracker won’t make your returns better, but it will tell you the truth about what’s happening. And for a lot of people, that clarity is what makes the difference between investing with confidence and investing with crossed fingers.

The spreadsheet detour

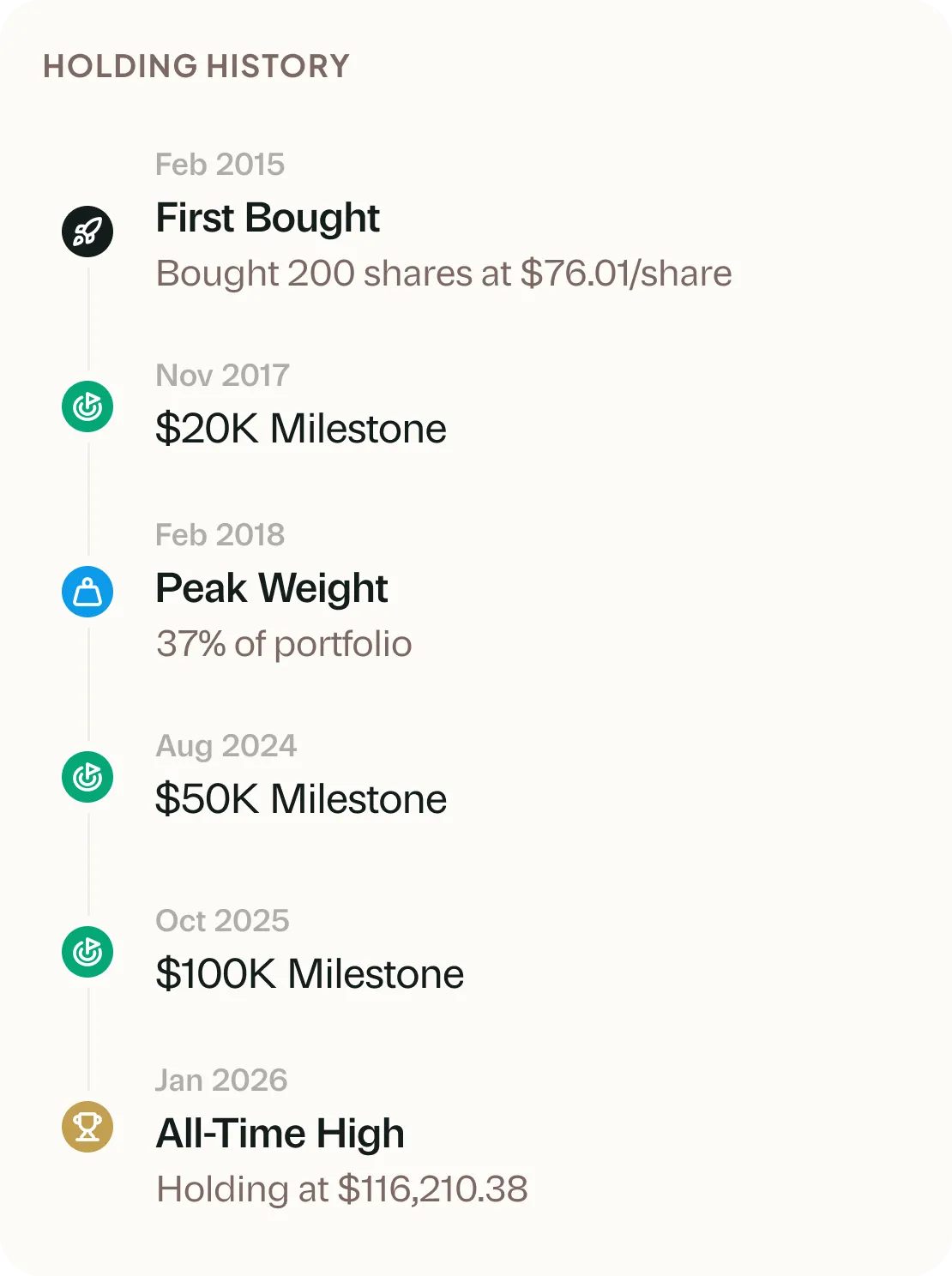

Almost everyone takes this detour. You decide you want to track things properly, so you build a spreadsheet. Columns for each account, rows for each holding, formulas for total allocation. It feels great for about three weeks. You update it diligently after every trade, colour-code the tabs, maybe even add a chart.

Then you miss a week. Then a month. Then you open it six months later and the data is so stale it’s useless. This isn’t a sign that tracking doesn’t matter. It’s a sign that manual tracking doesn’t stick. The impulse was right. You wanted to see your portfolio as one thing, not five separate accounts. The spreadsheet just wasn’t the right tool to get you there. If you’re coming from spreadsheets, you already know the value of seeing everything together. You just need something that doesn’t require you to maintain it by hand.

What if I only have $10,000 invested?

The dollar amount matters less than the complexity. If you have $10,000 in a single ETF inside one TFSA, your brokerage app handles that just fine. You can see the balance, you know what you own, and there’s not much to track beyond that.

But if that $10,000 is spread across three accounts, maybe a TFSA, an RRSP, and a small taxable account, the picture changes. You can’t see your combined allocation without logging into each one. You might be duplicating holdings without realizing it. And if you’re contributing to all three, knowing your real return across the board becomes nearly impossible from the individual apps alone. It’s not about the size of the portfolio. It’s about whether your current tools can answer the questions you’re starting to ask.

Is a portfolio tracker the same as a financial plan?

No, and it’s worth being clear about this. A portfolio tracker shows you what you own and how it’s performing. It answers questions like “what’s my asset allocation right now?” and “how did my portfolio do this year compared to the market?” It gives you a picture of where things stand today.

A financial plan is different. It tells you how much you need to save, what rate of return you need to hit your goals, and when you might be able to retire or buy a house. It’s forward-looking. A tracker is present-tense.

They’re complementary, not interchangeable. You can have a great financial plan and still have no idea what you actually own or how your portfolio performed last year. And you can have perfect visibility into your holdings without any sense of whether you’re on track for your goals. Most people benefit from both, but they solve different problems.

More in The Long Game

Best way to track your portfolio in Canada

What to look for in a portfolio tracker

Do you know how your portfolio is actually doing?

Best way to track your portfolio in Canada

We built a portfolio tracker, so we're biased. But here's an honest look at every approach: spreadsheets, brokerage tools, bank-linked apps, and more.

What to look for in a portfolio tracker

Do you know how your portfolio is actually doing?

See everything in one place

See your full portfolioFree during Beta. Early Members will be offered better rates than new users when we launch paid plans.